This planner won't give you the answer. But it might help you find it.

No tool, calculator, or spreadsheet replaces professional financial advice. If your situation is complex — a large DB pension, significant assets, divorce, inheritance — a good adviser is worth every penny. Many will tell you upfront whether you actually need them.

What this planner does is answer a simpler question: have I got enough?

It takes your pensions, ISAs, savings, and income sources, runs them through real UK tax calculations, and shows you what your retirement income could look like — based on what you tell it.

A word on financial literacy

The single best thing you can do before touching this planner is spend a few hours with the people who've been explaining this stuff for free, for years.

Pete Matthew at Meaningful Money, Pensioncraft, James Shack, Damian Talks Money. YouTube, podcasts, books. It's all there.

The more you understand your own money, the more useful this tool becomes.

You can find a curated list of the best free resources in the Resources section of the planner.

Setting expectations

It will show you whether your projected income covers your target across different scenarios and retirement ages.

It will not tell you how to invest, what funds to buy, or whether your strategy is optimal. For that you need an adviser or significantly more reading.

For couples, the planner pools income needs into a single target and draws from accounts in a defined order. It is a "do we have enough together" tool — not a tool for modelling two independent financial strategies within one plan.

The most important section in the planner

Get this right and everything downstream makes sense. Rush it and your projection will be telling you a story about someone else.

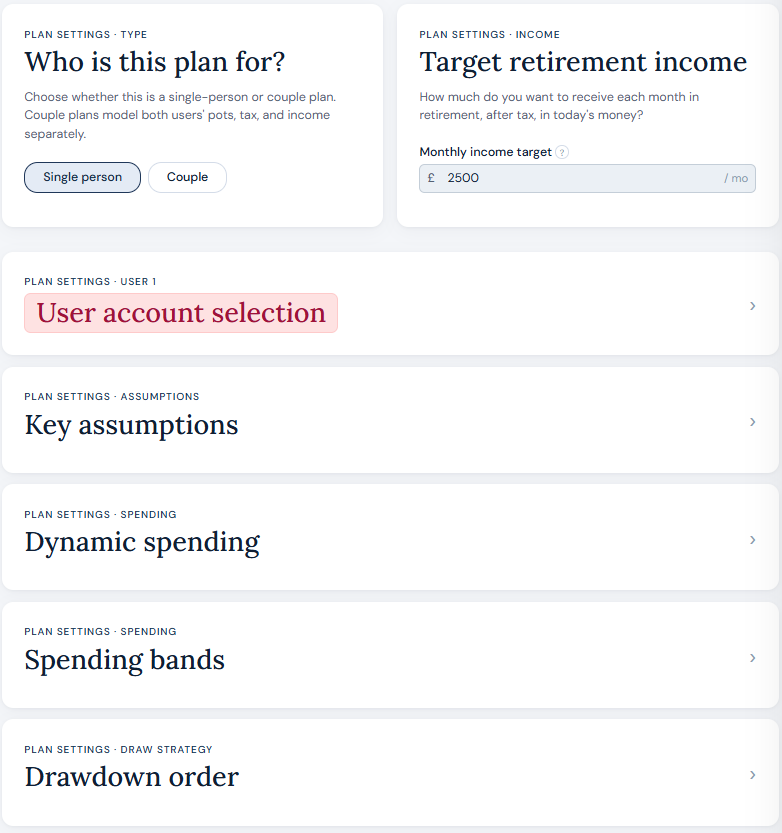

Who is this plan for?

Single or couple. Simple choice, significant difference in how the planner behaves.

Target retirement income

The monthly income you want to receive after tax, in today's money. Be honest with yourself here. Most people underestimate what they actually spend.

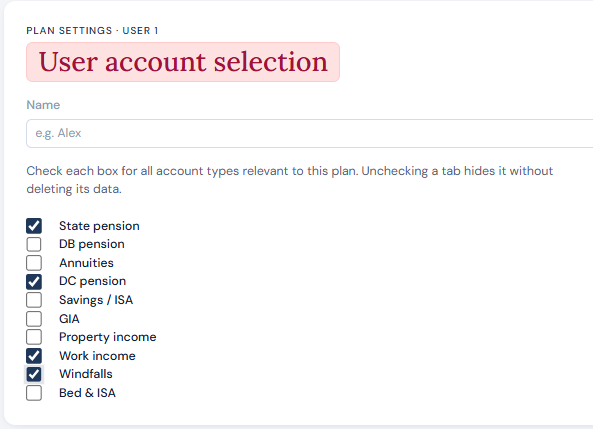

Users

Enter a first name for each person, or leave as User 1 / User 2. Then select which income sources and account types are relevant — DC pension, DB pension, ISA, savings. Only activate what applies to you.

Unchecking a tab hides it without deleting its data. If you don't have a particular account type but want to set a growth rate for it, create it with a zero balance.

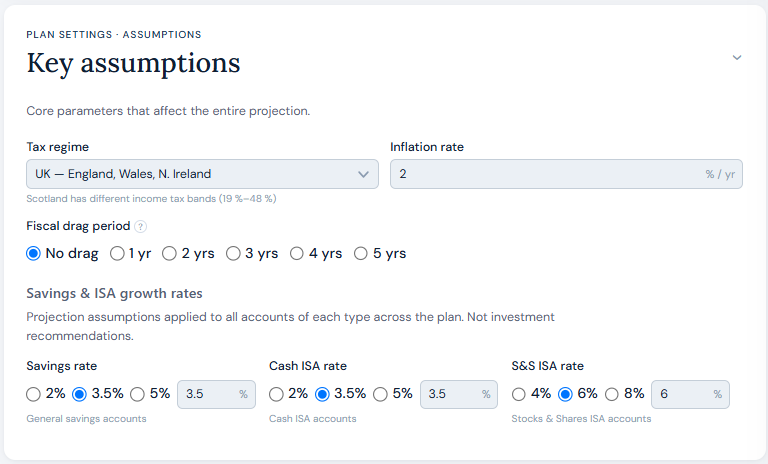

Key assumptions

This section has more impact on your projection than most people expect. Small changes here compound significantly over a 30-year retirement horizon.

Tax jurisdiction

England, Wales & Northern Ireland, or Scotland. Scottish income tax bands differ meaningfully and the planner models both correctly.

Inflation

Default 2%. Adjust if you have a strong view. A 1% difference compounded over 30 years has a material impact on your outcome.

Fiscal drag

The government has repeatedly frozen tax band thresholds in recent years, pulling more income into higher bands without technically raising rates. You can model up to 5 years of continued drag, or assume bands rise with inflation. Nobody knows which will happen. Model both and see the difference.

Run your baseline with "No drag" first, then re-run with 3 or 5 years of drag to see the income impact. Save each as a scenario to compare side by side.

Account growth rates

This planner is careful not to engage in financial advice. The selection of accounts based on growth rates is beyond its scope.

Savings and ISA growth rates are therefore set here based on your own determined average return for each account type. You can retain the default values for savings, cash ISA, and S&S ISA, or set your own. There is no right answer — these are your assumptions, not recommendations.

A high account balance paired with a high growth rate will have a material impact on your projected outcome compared to a more conservative figure. Consider the growth rates you use carefully, and be consistent — using the same assumptions across scenarios makes comparisons meaningful.

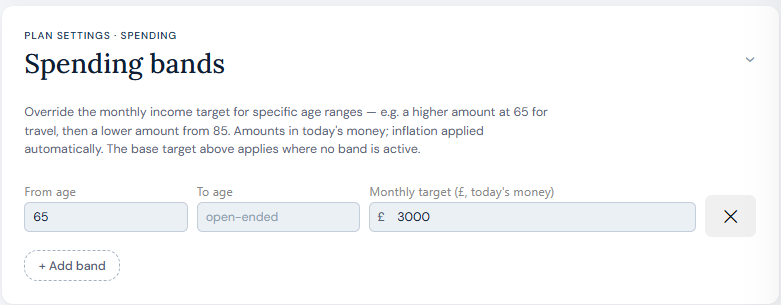

Spending bands

Lets you increase or decrease your income target for specific periods of retirement. More in the early years for travel and activity, less as you naturally slow down. A common and sensible approach to retirement modelling.

Amounts are in today's money; inflation is applied automatically. The base target applies where no band is active.

Leave this blank on your first run. Get your baseline projection first, then come back and layer spending bands in.

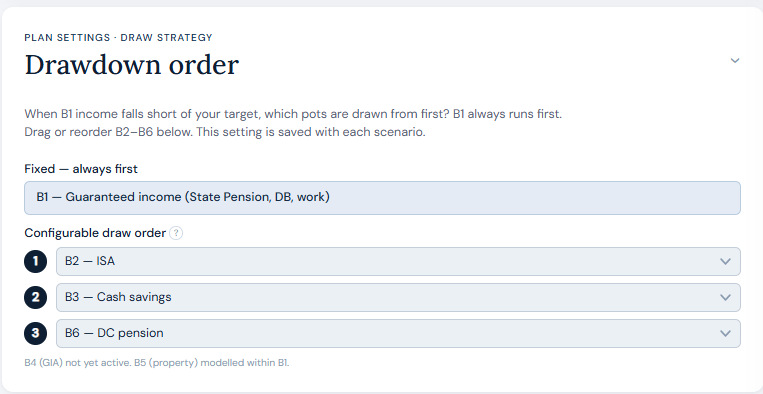

Drawdown order

Guaranteed income — state pension, DB pension, employment, annuities — is applied first against your monthly target. Whatever gap remains is funded from your flexible accounts.

You set the order in which those flexible accounts are drawn — ISA, savings, DC pension — with the first pot exhausted before the second is touched. A default order is provided but you can change it to suit your own tax planning priorities.

This setting is saved with each scenario, so you can model different drawdown sequences without losing your work.